Want To set up a company in India — Overview

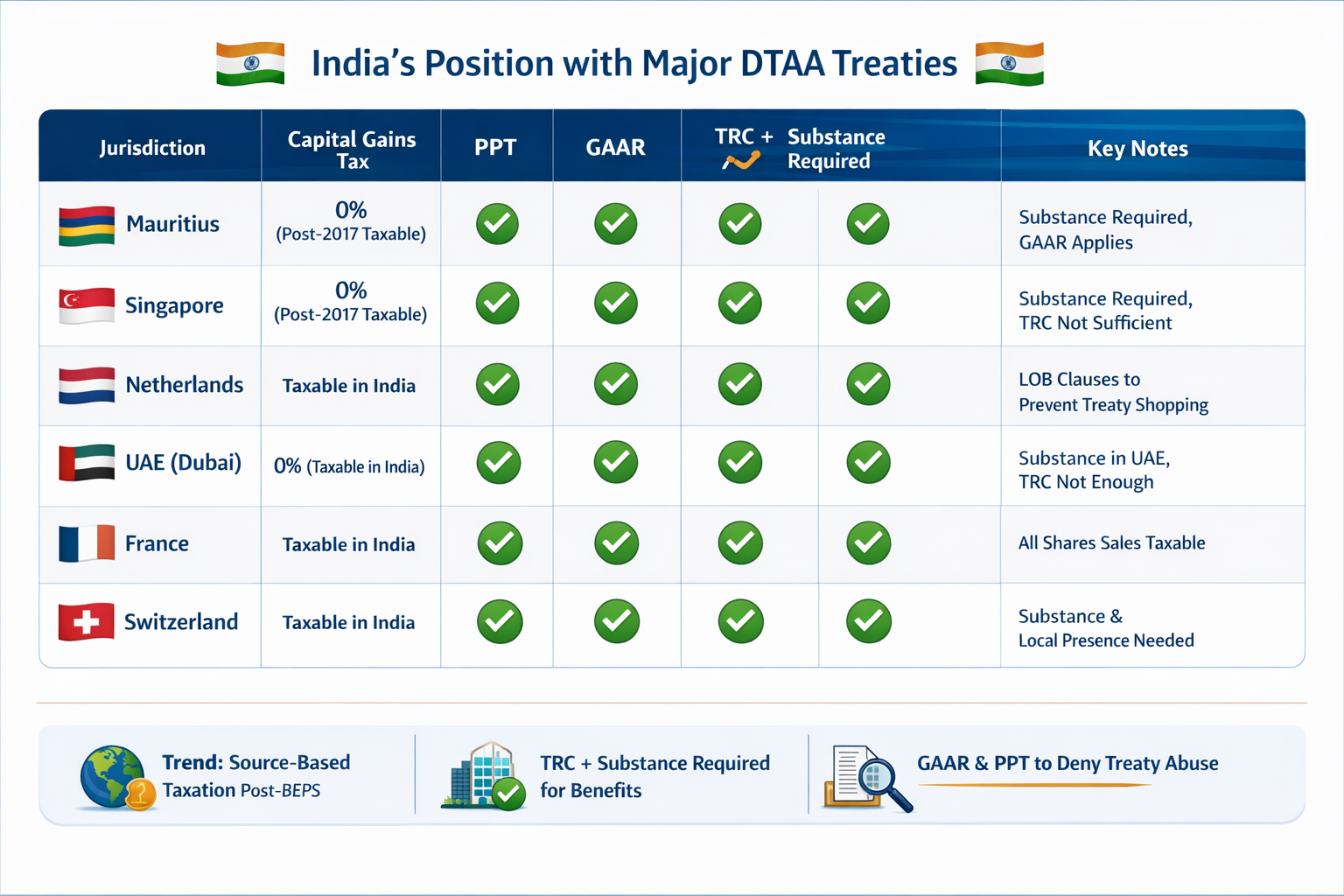

Comparison of India’s Position with Other Major DTAA Treaties after Tiger global Supremecourt Judgement

By Nagavarapu Sudheer, M.Com, F.C.S, L.L.B Partner, A2 Consultants

India–Mauritius DTAA

- Historically zero capital gains tax on share sales routed via Mauritius because Mauritius did not tax capital gains, making it a popular conduit for FDI into India.

- 2016/17 amendments gave India the right to tax capital gains on investments made after 01/04/2017.

- Following the Tiger Global ruling, India can deny treaty benefits where the structure is abusive or lacks substance, even if a Tax Residency Certificate (TRC) exists.

- The Principal Purpose Test (PPT) has been introduced to deny benefits where tax advantage is a main purpose.

Key India Mauritius Notes:

Treaty benefits not automatic

Substance requiredf

GAAR can override DTAA benefits.

India–Singapore DTAA

Like Mauritius, Singapore was also used as a treaty conduit for FDI due to favorable capital gains treatment.

- After treaty changes, India can tax capital gains arising from share transfers post 01/04/2017.

Similarities to Mauritius:

PPT applies

Substance standards increasingly required

No automatic relief based solely on TRC

India–Netherlands DTAA

- Traditionally standard OECD model based — India retains the right to tax capital gains on shares of Indian companies if substantial value is from India.

- Unlike the older Mauritius regime, Netherlands treaty never provided blanket capital gains exemption for investors.

Key Differences:

Less “conduit/misuse” advantage

Capital gains rights more source based

LOB clauses common to curb treaty shopping

India–France (Revised)

- Recent revision reduced dividend tax but expanded India’s capital gains taxing rights, making all share sales in India taxable regardless of threshold.

- Highlights a global trend: treaties being updated to balance investor relief with sovereign taxing rights.

Takeaway:

While treaties vary, a common global norm post BEPS/MLI is:

Capital gains rights tend to reside with source country,

Treaty benefits conditioned on substance and commercial rationale.

India–UAE (Dubai/Abu Dhabi) DTAA

- The UAE (including Dubai) is a popular holding jurisdiction due to zero capital gains tax and a flexible corporate environment.

- Treaty allows reduced withholding taxes on dividends, interest, and royalties, but capital gains from shares are taxable in India if the UAE entity lacks commercial substance.

- India now requires substance and economic reality, consistent with PPT and GAAR principles, to grant treaty benefits.

Key Notes:

TRC is necessary but not sufficient

Substance includes employees, office, and decision-making in UAE

Popular for PE/VC structuring, but must comply with BEPS/MLI norms

India–Switzerland DTAA

- Switzerland used for holding structures and family offices.

- Provides reduced withholding taxes but capital gains from Indian shares remain taxable if Swiss entity is a shell.

- Substance requirements include local employees, real office, and decision-making, similar to Mauritius and Singapore.

2) Checklist for Foreign Investors Building Treaty Based Holding Structures

To ensure DTAA benefits hold up under scrutiny — especially in India — investors should follow this checklist:

Legal and Structural Requirements

- Valid Tax Residency Certificate (TRC) from the holding jurisdiction.

- Proper incorporation and compliance with local company law (e.g., actual registered office).

- Limitation on Benefits (LOB) clause compliance if the treaty includes it (to avoid treaty shopping).

Substance & Operational Requirements

- Genuine board meetings with majority of directors physically participating in the treaty jurisdiction.

- Local decision making authority – strategic, financial, and investment decisions documented and taken locally.

- Real employees and payroll in the treaty jurisdiction.

- Local bank accounts and operational costs commensurate with economic activity.

- Commercial rationale beyond tax savings (e.g., business purpose for holding entity).

Why substance matters:

India now examines substance and rejects reliance on TRC alone where arrangements are primarily tax motivated.

Documentation & Record Keeping

- Minutes of meetings, evidence of decision making, strategic planning.

- Audit trails showing cash flows in and out of the entity.

- Evidence of commercial interactions (contracts, employee timesheets, office leases).

Tax & Treaty Compliance

- Advance Pricing Agreements (APAs) or Advance Rulings where appropriate.

- Regular legal audits to assess treaty eligibility under evolving BEPS/GAAR norms.

- Tax opinion letters supporting the structure’s commercial purpose.

- Review of treaty updates and MLI impacts regularly.

3) Practical Case Studies: Compliant vs Non Compliant Structures

Case A: Compliant Treaty Structure

Scenario:

A Singapore holding company legitimately runs its investment operations from Singapore and holds Indian portfolio investments.

Features:

Local Singapore employees and office space

Board meetings conducted in Singapore

Decisions on acquisitions, capital allocation, exits made by Singapore directors

Documented commercial strategy beyond tax

Outcome:

Strong defense against GAAR/PPT tests because substance, economic activity, and commercial rationale exist — not just a superficial shell.

Result:

Investor likely retains treaty benefits under India–Singapore DTAA (e.g., reduced withholding tax).

Key point: Token residency isn’t enough — actual business presence is required.

Case B: Non Compliant “Shell” Treaty Structure

Scenario:

A Mauritius entity incorporated solely as a conduit for tax benefit, with no real local operations, few or no employees, and strategic decisions taken abroad.

Features:

TRC obtained but no real substance

Board meetings held virtually from another jurisdiction

No local office, no payroll

Investment decisions documented elsewhere

Outcome:

Under India’s Tiger Global decision and GAAR/PPT doctrine, benefits denied because entity lacks commercial substance.

Result:

Capital gains taxed in India despite the treaty; investor faces tax plus interest/penalties.

Key point: Substance > documentation — legal form cannot replace economic reality.

Case C: Partial Compliance with Weak Documentation

Scenario:

A Cyprus holding company has an office lease and a couple of employees but major decisions are made by parent company executives overseas; limited evidence of local decision making.

Risk Factors:

• Weak evidence of board deliberations locally

• Major financial decisions by non resident managers

Outcome:

Tax authority may argue entity lacks effective management in treaty jurisdiction and deny treaty benefits.

Lesson:

Substance is not just paperwork — it must reflect real economic control locally.

Key Takeaways for Investors

Treaty reliance must be backed by substance — not just TRC or incorporation.

India and other countries now apply PPT/GAAR standards that allow denial of benefits if primary purpose is tax advantage.

Documentation/operations must demonstrate real business activities and decision making in the treaty jurisdiction.

Regular review of treaties, BEPS measures, and local case law is essential — treaty norms are evolving globally.

For detailed insights and practical guidance, visit our Knowledge Center and access our curated guides on India market entry: https://www.a2consultants.in/guides/international-taxation-in-india-for-foreign-companies

Nagavarapu Sudheer is a veteran tax and regulatory consultant at A2 Consultants with over 24 years of experience. A fellow member of the Institute of Company Secretaries of India (F.C.S) with a background in Law (L.L.B) and Commerce (M.Com), he has specialized in FDI structuring and group corporate restructuring for Fortune 500 companies and global startups alike. https://in.linkedin.com/in/sudheer-nagavarapu-4225334b

Need a Structural Review of your business prospects in India? > If you are looking to pounce on the FTA opportunity and looking to review your business prospects . [Contact A2 Consultants for a Private Consultation ] https://www.a2consultants.in/home/book_slot