India Entry: Wholly Owned Subsidiary vs. Joint Venture — Overview

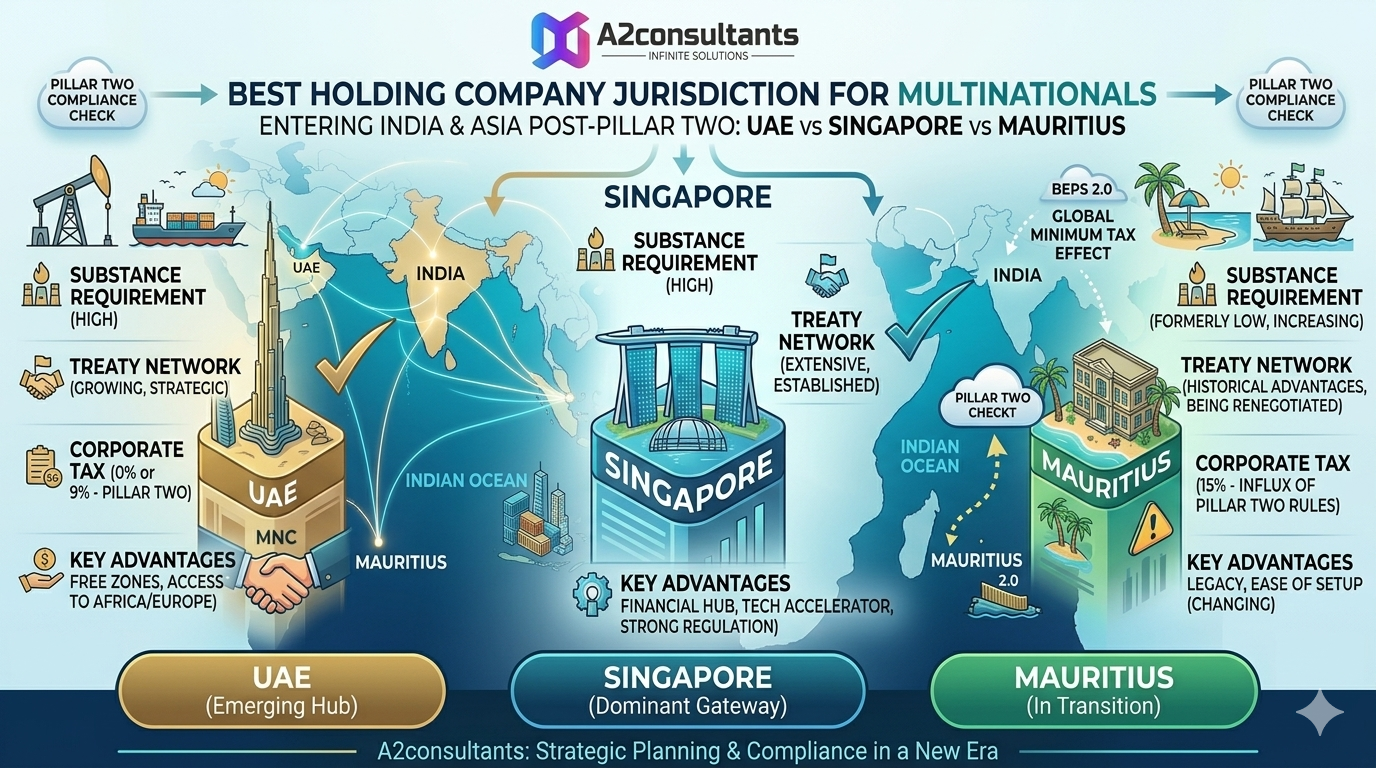

Best Holding Company for Multinationals Entering India Post Pillar Two | UAE vs Singapore vs Mauritius

By Nagavarapu Sudheer, M.Com, F.C.S., L.L.B., Partner, A2 Consultants

Introduction

For multinational enterprises (MNEs) with revenues exceeding €750 million and $ 800 million, the implementation of OECD BEPS 2.0 – Pillar Two (Global Minimum Tax) has fundamentally changed how cross-border structures are designed.

Historically, jurisdictions like Mauritius, Singapore, and UAE were used for and in our experience, it was primarily Singapore was used for the Asia pacific region:

- Tax-efficient holding structures

- Dividend routing

- Capital gains optimization

However, with a 15% global minimum tax, traditional tax arbitrage is no longer the primary driver.

Today, the key question for MNCs entering India and the broader Asian market is:

Which jurisdiction offers the best combination of tax efficiency, treasury flexibility, regulatory ease, and strategic positioning under Pillar Two?

This article compares UAE, Singapore, and Mauritius from a post-Pillar Two perspective and identifies the optimal structure for India/Asia entry.

Pillar Two – What Changes for India/Asia Entry Structures?

Under Pillar Two:

- MNEs (>€750M or $800M) must pay minimum 15% effective tax rate (ETR)

- If a jurisdiction taxes below 15%: A top-up tax applies (locally or at parent level)

Key Implication for Holding Structures:

Low-tax jurisdictions like Mauritius or UAE no longer provide pure tax arbitrage benefits for large MNEs.

Instead, structuring decisions must now focus on:

- Withholding tax efficiency

- Capital flow flexibility

- Treaty benefits with India

- Treasury and regional expansion strategy

- Regulatory credibility and substance

Jurisdiction Comparison: UAE vs Singapore vs Mauritius

1. Tax & Pillar Two Impact

Jurisdiction, Headline Tax, Pillar Two Impact

UAE Tax 0% (Free Trade zones ) / 9% Adjusted to 15% via DMTT

Singapore Tax 17% Effective ~15–17%

Mauritius 15% (with exemptions) Effectively aligned near 15%

Insight:

All three jurisdictions converge around 15% ETR, removing tax rate advantage.

2. India Treaty Benefits (CRITICAL FACTOR)

Mauritius

- Historically strong India treaty

- Capital gains benefits significantly reduced post-2017

- Still useful for: Debt structures Certain fund structures

Singapore

- Strong India treaty

- Capital gains exemption (subject to conditions)

- Widely accepted by tax authorities

UAE

- India-UAE DTAA provides: 0% capital gains (in many cases) No withholding tax in UAE

Insight:

- Singapore & UAE now preferred over Mauritius for equity investments into India, the rest of Asian countries depending on the country we need to ponder on the DTTA provisions to understand the best suited.

3. Treasury & Capital Flow Efficiency

UAE

- No withholding tax

- Free repatriation of funds

- No FX restrictions

- Ideal for: Dividend routing Regional cash pooling

Singapore

- Advanced treasury ecosystem

- Strong banking and hedging infrastructure

- Ideal for: Global treasury centres Structured investments

Mauritius

- Moderate flexibility

- Banking ecosystem less sophisticated

- Often used for: Investment holding (not treasury hubs)

Verdict:

- Best Treasury Hub winner is Singapore

- Best Capital Flow Flexibility winner is UAE

4. Regulatory Credibility & Substance

Singapore

- High global credibility

- Strong substance requirements

- Preferred by institutional investors

UAE

- Improving rapidly

- Strong for commercial operations

- Still perceived as lower substance vs Singapore

Mauritius

- Increasing scrutiny globally

- Substance requirements strengthened

- Perception has weakened post-BEPS

Insight:

- For large MNEs Singapore strongest

- Mauritius faces credibility challenges

5. Ease of Doing Business

UAE

- Fastest setup

- Low compliance burden

- Business-friendly environment

Note: In our experience the cost of setting up and running a company in UAE has gone substantially high and the low compliance burden is a thing of the past.

Singapore

- Efficient but structured

- Higher compliance than UAE

- Strong governance

Mauritius

- Simple structure

- Lower operational complexity

- Limited ecosystem depth

Strategic Structuring for India Entry

Pre-Pillar Two Model:

- Mauritius holding → India investment

- Tax-driven structuring

Post-Pillar Two Model:

Structure must align with commercial substance + treasury + regional strategy

Recommended Structures

1. UAE Holding Structure (Best for Flexibility) for small and medium companies

Ideal for:

- Promoter-led groups

- Middle East / India corridor

- Dividend and capital flow efficiency

Advantages:

- Zero withholding tax

- Strong treaty with India

- Flexible capital movement

Limitation:

- Requires strengthening of substance for large MNEs

2. Singapore Holding Structure (Best Overall for MNCs)

Ideal for:

- Institutional investors

- Asia-Pacific expansion

- Treasury and investment platforms

Advantages:

- High credibility

- Strong treaty network

- Advanced financial ecosystem

Limitation:

- Higher cost of operations

3. Mauritius Holding Structure (Niche Use Case)

Ideal for:

- Debt investments into India

- Fund structures

Advantages:

- Simple setup

- Some treaty advantages

Limitations:

- Reduced tax benefits post-2017

- Lower global acceptance

Final Recommendation: What is the Best Country?

Rank 1 Singapore – Best for Large Multinationals

- Strongest balance of: Tax alignment (Pillar Two compliant) Treasury capabilities Regulatory credibility

Rank 2 UAE – Best for Flexible & Efficient Structures

- Excellent for: Capital flow optimization Regional HQ structures Promoter-driven investments

Rank 3 Mauritius – Limited Strategic Relevance

- Useful only in: Specific fund or debt structures

- No longer preferred for mainstream India entry

Conclusion

Pillar Two has shifted the focus from low-tax jurisdictions to strategic jurisdiction selection.

For multinationals entering India and Asia:

- Singapore emerges as the most robust and future-proof holding jurisdiction

- UAE complements as a high-flexibility regional hub

- Mauritius is now a niche jurisdiction with limited strategic role

The winning structure is no longer tax-driven — it is strategy-driven, substance-backed, and treasury-optimized.

Nagavarapu Sudheer is a veteran tax and regulatory consultant at A2 Consultants with over 24 years of experience. A fellow member of the Institute of Company Secretaries of India (F.C.S) with a background in Law (L.L.B) and Commerce (M.Com), he has specialized in FDI structuring and group corporate restructuring for Fortune 500 companies and global startups alike. https://in.linkedin.com/in/sudheer-nagavarapu-4225334b

Need a Structural Review of your business prospects in India? > If you are looking to pounce on the FTA opportunity and looking to review your business prospects .

[Contact A2 Consultants for a Private Consultation ] https://www.a2consultants.in/home/book_slot