Want To set up a company in India — Overview

TRC and GAAR Rules in India: Tax Residency Certificate & Anti-Avoidance Explained

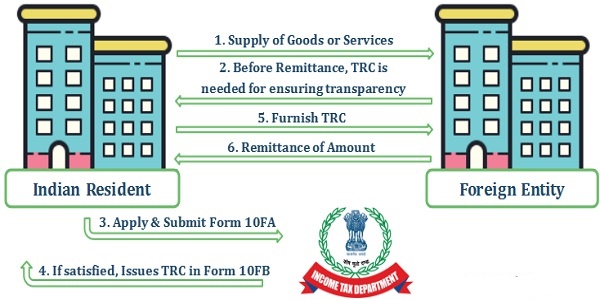

A Tax Residency Certificate proves that a person or company is a tax resident of a particular country. For example: An Indian resident claiming DTAA benefit must show they are a resident of India. This certificate is issued by the Income Tax Department of India.

Why TRC is Required

Under Section 90(4) of the Income-tax Act, DTAA benefits cannot be claimed without a TRC.

It is required to:

-

Apply reduced withholding tax rates

-

Claim foreign tax credit

-

Prove treaty eligibility

How to Obtain TRC in India

Indian residents apply online through the Income Tax Department of India portal. Form 10FA – Application for TRC. TRC issued in Form 10FB

Earlier, having only a Tax Residency Certificate (TRC) was often enough to claim treaty benefits under the India–Indonesia Double Taxation Avoidance Agreement. But now TRC alone is NOT sufficient because of anti-avoidance rules.

Two major rules apply:

-

General Anti-Avoidance Rule (GAAR)

-

Principal Purpose Test (PPT) under the OECD BEPS framework.

Why TRC Alone Is Not Enough

Authorities want to ensure the company really operates in that country and is not just a shell used for tax benefits. Even if a company has a TRC, tax authorities may deny treaty benefits if:

-

The entity is a paper company

-

The structure is created mainly to avoid tax

Example

Earlier many investors used Singapore companies to invest into Indonesia instead of investing directly from India. Singapore treaties sometimes offered better capital gains or dividend tax treatment. The Singapore company would obtain a TRC and claim treaty benefits. Under PPT, authorities ask:

Was the main purpose of the structure to obtain a tax benefit?

If the answer is yes, treaty benefits can be denied even if:

-

TRC exists

-

Company is legally incorporated

If Indian promoter sets up:

-

Singapore company

-

No office

-

No employees

-

No business activity

But uses Singapore only to invest into Indonesia. Even with a Singapore TRC, authorities may say:

-

Structure exists only for tax advantage

-

DTAA benefit denied

So Indonesian domestic tax applies.

To successfully claim treaty benefits, the intermediary company should have:

1. Office in the country

2. Local directors

3. Employees

4. Bank accounts

5. Business operations

6. Decision-making happening there

This proves commercial substance.

GAAR Impact in India

Under General Anti-Avoidance Rule (GAAR), the Income Tax Department of India can disregard arrangements whose main purpose is tax avoidance. The following additional documents are now required along with TRC

1. Form 10F

Form 10F is a declaration required under Indian tax rules when claiming DTAA benefits if all required details are not fully mentioned in the TRC.

It contains information such as:

-

Name of the taxpayer

-

Status (individual/company)

-

Nationality or country of incorporation

-

Tax Identification Number (TIN)

-

Period of tax residency

-

Address in the country of residence

2. Beneficial Ownership Declaration

A beneficial owner is the person or entity that actually controls and enjoys the income, not just an intermediary receiving it temporarily. Tax authorities require a declaration confirming that the recipient is the true economic owner of the income.

3. Commercial Substance Proof

Tax authorities check whether the entity claiming treaty benefits has real business presence in that country.

4. No Treaty Shopping Structure

Treaty shopping means routing investments through another country only to obtain tax advantages under a treaty. Many countries now apply the Principal Purpose Test (PPT), which denies treaty benefits if the main purpose of the arrangement is to obtain tax benefits.

For detailed insights and practical guidance, visit our Knowledge Center and access our curated guides on India market entry: https://www.a2consultants.in/guides/india-market-entry-strategies-for-foreign-investors

Need a Structural Review of your business prospects in India? > If you are looking to pounce on the FTA opportunity and looking to review your business prospects . [Contact A2 Consultants for a Private Consultation as we have lot of European clients whom we are aleady helping in their business in India] https://www.a2consultants.in/home/book_slot